Introduction

In recent years, there has been a shift from investing in actively managed investment products such as mutual funds and hedge funds to investing in passive index funds such as S&P 500 index funds. This has been in large part due to the fact that there has been significant research that shows that the vast majority of actively-managed products do not beat the S&P 500 index in the long run after fees. However, the point of this article is to explain to you why I am only invested in individual stocks and closed-end funds that I research, the vast majority of which are small caps, and why I do not currently own an S&P 500 index fund.

Analysis of Investing in an S&P 500 Index Fund Right Now

One popular valuation metric for valuing the S&P 500 is the Shiller P/E ratio which was popularized by Robert Shiller, an economist at Yale. The ratio is the inflation adjusted price of the S&P 500 index at a point in time divided by the average of the trailing ten years inflation adjusted earnings. This Price to Earnings ratio is meant to adjust for what stage in the economic cycle the economy is currently in. For example, the economy may be booming and earnings may be high so a trailing twelve month price to earnings ratio would be low. But prospective returns may not be high because the economy may be at the end of the cycle. Earnings would decrease when the economy slows down.

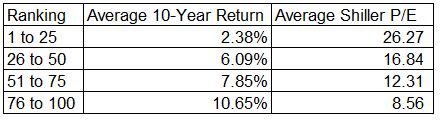

I have taken Robert Shiller’s data which is publicly available on his website and have done some calculations for the years from 1910 to 2009. For each year, I have calculated 10-year real returns and have taken the Shiller P/E ratio for each year from his file. (Although in Shiller’s data set, he uses the average daily closing price for each month so real returns will not be perfectly accurate for each year, my results will be close enough to make my point). I have ranked each year from one to 100 by Shiller P/E with one being the year with the highest Shiller P/E. Please see the table below for the results:

What is notable is that for each of the four categories as the Shiller P/E declines the average 10-year real return increases. According to Shiller’s website, the current Shiller P/E ratio is 30.04. I have taken the average of all years in my population with a Shiller P/E above the current Shiller P/E of 30.04. Here are my results:

From both of these tables, we can conclude that if the market deserves the same Schiller P/E multiple as it has been given in that past, then based the current multiple of 30.04 the market’s expected returns should be low. But one consideration that I think is valid is that the current market with a Shiller P/E of 30.04 may produce higher returns than past data would predict. There are more technology companies that are capital-light and can grow quickly and may deserve a higher multiple on earnings. But the question is how much higher should a fair Shiller P/E value be to compensate for the increase in the aggregate market capitalization of these kinds of businesses? It seems to me to answer this question would involve much more work than performing research and valuing individual small cap stocks. Right now, an investment in an S&P 500 index fund does not seem compelling because of the difficulty in determining what expected real returns should be for the S&P 500 going forward at the current multiple of 30.04 Historical data would suggest real returns of around -0.91%.

The Case for Investing in Small Caps

In recent years, there was a study published Martijn Cremers called Active Share and the Three Pillars of Active Management: Skill, Conviction and Opportunity. The study concludes that fund managers with very high active share are more likely to outperform and a small-cap strategy would have a very high active share. But first let me explain how to calculate active share. Active share is calculated by taking the % allocation of your fund in a position and subtracting the % allocation of this position in the S&P 500 index. You add all of these differences up to get your active share. So for example if you owned a one stock portfolio which was 100% invested in Microsoft and Microsoft had a 3% allocation in the S&P 500 index then your portfolio would have a 97% active share. Small cap stocks are not included in the S&P 500 so a small cap portfolio would have a very high active share. One conclusion of the study is that small cap funds with both high active share and a long fund holding duration (both factors being in the top-quartile of the study) generated an annualized alpha (or in layman’s terms outperformance) of 1.94%, which was statistically significant.

Intuitively, this result of this survey makes sense to me because of the rise in investing in index funds in recent years. An investment in an S&P 500 index fund in increases the value of companies by market capitalization (the index is weighted by market capitalization) without taking into account other factors such as fundamentals and valuation. Many small cap companies that are cheap and have good fundamentals may be left behind in the rise of the S&P index fund. This creates opportunities for smaller funds and individual investors.

Conclusion

I own individual small cap stocks and don’t invest in the S&P 500 index for several reasons. The Shiller P/E ratio is high right now and based on a historical analysis of 10-year real returns for years with higher Shiller P/E ratios, expected real returns for the next ten years may not be high. If the market deserves to be valued at a higher Shiller P/E ratio, it would be hard to quantify how much higher and therefore would be hard to forecast expected returns. In contrast, small cap stocks are easier to value than the S&P 500. There is also data that shows that small cap funds which have high active share and a longer holding period outperform the market. This makes sense to me because small caps would not be included in an S&P 500 index and their prices would not rise as money flows into S&P 500 index funds. Therefore, there should be more opportunity for individual investors and some small funds to invest in cheap small cap stocks with good fundamentals.

Disclaimer

The views on this site are mine and do not necessarily represent the position of my employer.