Intelligent Investor Excerpt

In 1949, Benjamin Graham, the Columbia Business School Professor most credited with shaping Warren Buffett’s investing philosophy, wrote his first edition of the Intelligent Investor, his well-known work for how to invest in the stock market. One of his recommended investments was investing in closed-end mutual funds at a discount to NAV (net asset value) of greater than 10%. A closed-end mutual fund has a fixed number of shares and as a result the price of these shares can trade at a premium or discount to the underlying assets minus liabilities held by this mutual fund. In the Intelligent Investor, Benjamin Graham promotes investment in closed-end mutual funds at a discount using a simple example. Investor A buys a open-end fund at a 9% premium while Investor B buys a closed-end fund at a 15% discount. Both investors pay a 1.5% commission. Both funds pay out 30% of the NAV as dividends and end up with the same NAV as the beginning of the period after four years. Investor A earns a 21% return on his investment (30%distribution-9%premium). For Investor B to earn the same return as Investor A, the discount in Investor A’s shares would have to widen from 15% to 27%. Therefore, buying closed-end mutual fund shares at a discount offer better prospects for returns than buying open-end shares at a premium.

Introduction

180 Degree Capital is a closed-end mutual fund that is trading at a roughly 30% discount to NAV. The mutual fund focuses on investing in micro-cap companies (companies with a market capitalization of less than $250 million) which is a segment of the market with little competition. The mutual fund is run by a portfolio manager with 17 years of experience running high performing funds at Blackrock, Kevin Rendino. He has spent a significant portion of his after tax salary from 180 Degree Capital purchasing its shares and has high insider ownership. At 180 Degree Capital, Kevin Rendino has instilled an impressive investment process and practices varying degrees of investor activism when necessary. Although the fund trades at a discount, I think because of what area of the market it focuses on and its experienced portfolio manager it is poised to compound NAV at relatively high rates.

Company History

Before Kevin Rendino became CEO, 180 Degree Capital was formerly known as Harris and Harris Group. It was a business development company that focused on investing in private investments. As detailed in Rendino’s first letter to shareholders as CEO, expenses at the BDC were high and performance was mediocre. With the company’s high cost structure at the time, it would have been forced to liquidate private investments just to fund its expenses. He restructured the company as a closed-end mutual fund that would begin to liquidate its private investments when possible at the right prices and reinvest the proceeds in micro-cap public investments. In his first letter to shareholders (Q2 2017), Kevin Rendino details how he immediately began to cut operating expenses from a five-year average of $1.6 million per quarter to $1.05 million in Q1 2017 and to $735,000 in Q2 2017. A significant way in which he reduced expenses was by moving the office from Manhattan to Montclair, NJ.

Experienced Portfolio Manager with Significant Insider Ownership

Before taking over as CEO of 180 Degree Capital, Kevin Rendino had over twenty years of experience running the Basic Value Fund at BlackRock and Merrill Lynch. Before leaving Blackrock, he led their value investing strategies and oversaw 11 funds with $13 billion in assets under management. During his career for the funds that he managed he beat the S&P 500 by over 100 basis points. This is especially impressive considering the amount of money that he managed. Since taking over as CEO of 180 Degree Capital, Kevin Rendino has invested a significant portion of his after-tax compensation back into the fund.

As of his latest filing, Rendino owns a total of 642,214 shares worth roughly $1.4 million dollars. As his insider ownership is high and he continues to purchase shares, Kevin Rendino’s interests should be aligned with other investors in the fund. It is unlikely that he will attempt to raise too much money to generate higher fees at the expense of performance.

Microcap Focus

It is easier for a fund to generate higher performance by focusing on investing in microcap stocks because there is not as much competition as there is in other areas of the market. According to a chart from TURN’s investor presentation there is little equity research analyst coverage on microcap stocks:

According to the chart only 2.2% microcap stocks are covered by analysts versus 22.5% of stocks with market caps of greater than $12 billion. Furthermore, most hedge funds and mutual funds do not focus on investing in microcap stocks because of the fixed costs associated with running these funds and the high operating leverage of these businesses. The incentives of hedge fund managers and mutual fund managers are not always aligned with those of investors as managers are rewarded for maximizing assets under management as they are paid a fee as a percentage of assets under management. Generally, microcap funds work well when the portfolio manager has a significant portion of his or his family’s money invested in the fund and is not overly focused on generating higher fees. This is the case for 180 Degree Capital as Kevin Rendino has invested a significant portion of his after-tax salary from 180 Degree Capital into the fund.

Investment Process

Typically sophisticated investors in mutual funds have a strong focus on the investment process of these funds and I would characterized 180 Degree Capital’s investment process as robust. Here is an excerpt detailing its investment process from an investor presentation:

Typically a mutual fund doesn’t have a big enough research staff to cover every company in its investable universe and has to narrow its focus using stock screeners. 180 Degree Capital runs two level of screeners: 1) a screen that focuses on microcap companies based in the US and traded in the US 2) screens based on valuation metrics. The Portfolio Manager continues to whittle down his list of names by doing slightly more fundamental analysis until his list is down to 30-40 companies. This is a manageable number of names to do deep dive primary research on which includes calling customers, competitors, suppliers, and visiting with the company. The fund then typically invests in ten to fifteen of these companies. Recently, 180 Degree Capital hired another employee on the research team and this should strengthen the research process by adding additional depth to their research and/or increasing the number of companies they can cover well.

Performance

Since Kevin Rendino took over as CEO, the performance of public investments has been excellent and has outpaced all relevant indices. Please see the below excerpt from the company’s latest call slides:

Because the fund initially started with a high percentage of private investments that have not performed as well as its public investments, the increase of the fund’s NAV so far has not been as impressive as the performance of its public investments. Please see the below excerpt from the company’s latest call slides:

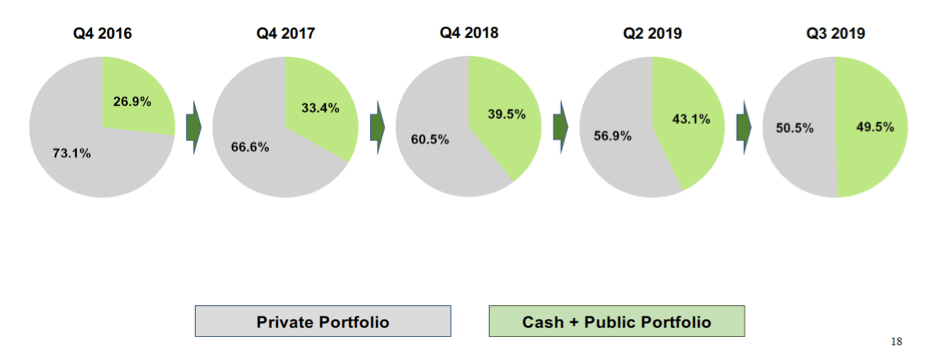

As a result of the outperformance of the public investments, the mix of public to private has also shifted to having a greater percentage of public investments. Therefore, the performance of the fund’s NAV should be higher going forward. Please see the below excerpt from the company’s latest call slides:

Example of Successful Investment – TheStreet (Ticker: TST)

In April 2017, 180 Degree Capital begun performing deeper due diligence on TheStreet and began conducting in-person meetings with management. The investment thesis was that the management team, which had been put in place two years prior, was strong and had experience turning around similar companies, MarketWatch and USA Today. But there was one key issue that was creating an overhang on the stock: a $55 convertible note that charged high rates of interest and had senior liquidation preference to common shares. From April to July 2017, 180 Degree Capital purchased 1 million shares of TST at an average price of $0.89 per share and in May began to present its ideas to management. In Q4 2017, 180 Degree Capital lead a round of $7.85 million in equity at $1.10 a share as part of an effort to help remove the overhang from the preferred shares. $4 million was directly from 180 Degree Capital and the other $3.85 million was raised by 180 Degree Capital in an SPV specifically for investing in TST. In Q4 2017, 180 Degree Capital and TST worked together to retire the $55 million in preferred stock for $20 million in cash and $6 million in unregistered shares of TST’s common stock. 180 Degree Capital at this point had enough shares to appoint a director to TST’s board as long as it didn’t sell any shares. 180 Degree Capital modelled that TST would trade at $1.38 without multiple expansion and at $1.96 with reasonable multiple expansion. In Q1 2019, 180 Degree Capital worked with TST to sell its B2B business to Euromoney, unlocking additional value. Finally in Q3 2019, 180 Degree Capital worked with TST to sell the remaining business to TheMaven. After exiting the investment, 180 Degree Capital recognized a 75% annualized IRR on its investment. It had a $7.2 million dollar gain on an initial $5 million dollar investment. The implied price per share of its exit price was $2.59 per share which was well above the most optimistic case in its model.

Valuation

My valuation is simple. The Q3 2019 NAV was 3.05 per share and the price per share as of this article was 2.10. I think that TURN should trade at 100% of its NAV. For a long term investor in this closed-end fund, there should be a significant appreciation in NAV over time as well as the narrowing or elimination of the roughly 30% discount to NAV.

Catalysts

Catalysts are events that cause securities that are undervalued to become fully valued. Here are catalysts that will narrow or eliminate the large discount to NAV:

- Monetization of private investments-There is a lot of uncertainty with how private investments will be exited. A couple of private investments are not too far from the stage in which they would IPO. If TURN can exit some of these investments because of IPO’s at fair valuations then the discount should narrow. TURN has also been able to sell some of its private investments at fair valuations in secondary offerings. If TURN is able to sell more of these investments in secondary offerings the discount should narrow.

- Continued Outperformance of Public Investments-If TURN’s public investments continue to rapidly appreciate the percentage of public investments out of the total portfolio should continue to increase and the discount should narrow.

Risks and Mitigants

I’ll list the risks related to the investment that I’ve identified below and some factors that mitigate these risks:

- Concentration of the public portfolio

- Risk-The public portfolio is designed to only have ten to fifteen investments at one time and there is a heightened chance of increased volatility or even larger losses if bad investment decisions are made

- Mitigants-A small cap fund usually has to manage its volatility because if enough investors redeem during a downturn in performance, the fund would have to sell holdings in which it has a large stake. This in turn could cause the holdings to depreciate further and could cause more redemptions. As TURN is a closed-end fund, investors cannot redeem their money and this should allow TURN to weather volatility. As Seth Klarman writes in his legendary value investing book, Margin of Safety, volatility should not be viewed as a measure of risk. A more apt measure of risk is the risk that your estimate of intrinsic value on an investment is written down and that your capital in the investment is permanently impaired. The risk that a bad investment decision is made which would have a greater impact on performance is mitigated by the fact that the investment team will have a greater knowledge of the investments it owns. It will have fewer investments to deeply research and this increased knowledge should mitigate the risk that a bad decision will be made.

- Monetization of Private Investments

- Risk-The private investments are illiquid and may never be monetized. It’s possible that these investments will not IPO, will not be bought out in a merger, will not be sold through a secondary transaction, and could become worthless.

- Mitigant-The risk that these investments could become worthless is mitigated by the steep implied discount that they’re trading at. At Q3 2019, assuming that the public investments and cash should be valued at 100% of NAV, the implied value that the market was giving to the private portfolio was $20.8 million while the private portfolio was valued at $49.3 million. This implies a discount of 58% on the private portfolio. I think it is unlikely that these assets will eventually be monetized at less than a 58% discount to their current value. And I think there is a strong possibility that TURN exits these positions for more than the $20.8 million implied value that the market is ascribing to them.

Disclaimers

1) The views expressed on this site are mine and do not necessarily represent my employer’s position.

2) I do not hold a position with the issuer such as employment, directorship, or consultancy.

3) I hold a material investment in the issuer’s securities.